A variable mortgage is a mortgage whose interest rate is not fixed and is referenced to a (…)-“> variable mortgage has been the star among those who wanted to buy a home reaching nearly 98% of the total 10 years ago but it was as a result of the arrival of the negative Euribor when banks focused all their commercial efforts on fixed mortgages since paying interest on debts does not go very well with your business.

It was in 2016 when the trend was beginning to become clear and in December of that year fixed mortgages already accounted for more than 32% of the total and increasing month by month until March 2021 when variable mortgages were only the 47% compared to 53% of the fixed ones. Without hardly noticing it and very little by little the banks had gotten away with it and they sneaked a product into us that at the moment is worse for customers. The maximum number of fixed mortgages we had in April of this year when they took 58.5% of the market, coinciding with a mortgage war and everything seemed to indicate that the trend was going to continue like this.

But something happened in May, clients may have realized that no matter how good a Fixed Mortgage is-

The current mortgage offer could be divided into three types, fixed, variable and mixed, being (…)-“> 1% fixed mortgage is still better a variable with the Euribor at -0.5% and looking like it will be hovering around zero for many years and it was in May of this year when we could say that the Bubble-

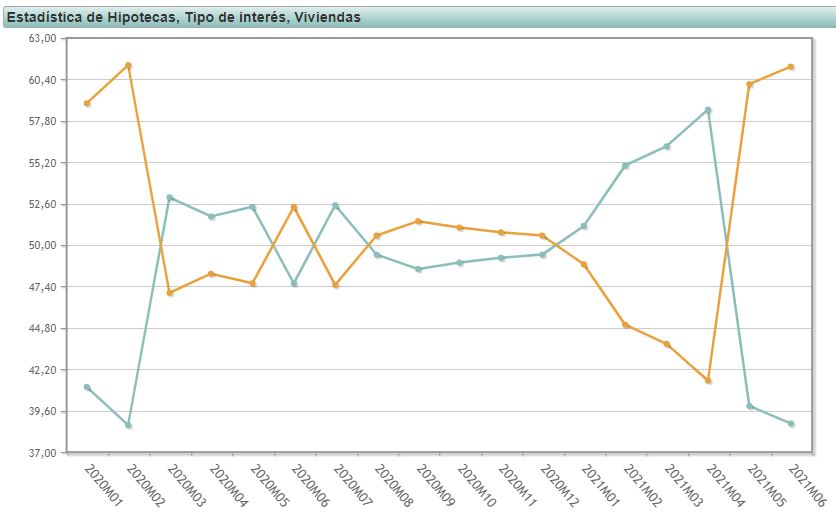

In economic terms, a bubble is a high volume of trade at prices that are (…)-“> The bubble of fixed mortgages exploded and fell in one month from a market share of 58.5% to 39.9%, a trend that continued the following month (the last for which we have data) when it fell to 38.8%.

In this graph you can see the evolution of variable mortgages versus fixed mortgages since January 2020.

The panorama has changed radically in a very short time and although it is probably a question of a relaxation in commercial policies, banks have realized that they cannot lower interest rates any further-

Interest rates are the levels at which interest is charged to a borrower for (…)-“> interest rates that they offer to their clients after the intense commercial battle. Even some banks have begun to slightly increase the price of fixed mortgages with which we could conclude that the fixed rate bubble has burst.

Despite the fact that the traditional mortgage business is bad for banks since the interests received (and even paid in some variables) do not compensate for the risk taken, the business has moved towards Linked Products-

Generally, banks offer two options in the mortgage offer, one with (…)-“> linked products, those financial products that you have to contract with the bank to benefit from the best conditions and that is where the banks’ business really is. The interest is that you take out home and life insurance and direct your payroll with them.