10.10.2024 – 00:30

comparis.ch AG

{kind=link}

A document

- 20241010_MM_Hypobarometer Q3_DE.pdf

PDF – 438 kB

Media release

Comparis mortgage barometer for the third quarter of 2024

Long-term fixed-rate mortgages are in high demand

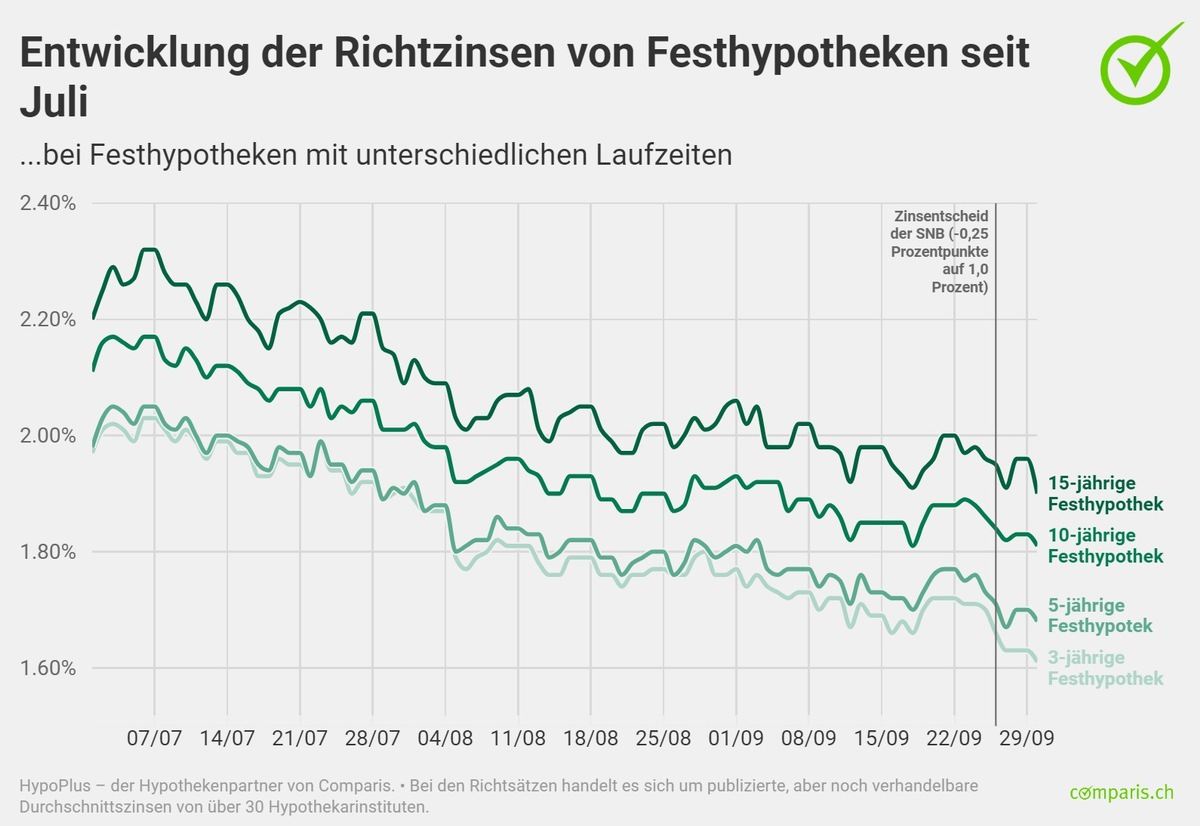

As expected, the Swiss National Bank (SNB) has lowered its key interest rate by 0.25 percentage points to 1 percent for the third time in a row. Declining inflation rates and market expectations that interest rates will continue to fall have already significantly reduced the conditions for fixed-rate mortgages from June and in the following months. 10-year fixed-rate mortgages were recently offered for an average of around 1.5 to 2.0 percent, while Saron mortgages cost around 1.6 to 2.0 percent after the interest rate cut. Long-term fixed-rate mortgages were particularly in demand in the third quarter. “The conditions for 10-year fixed-rate mortgages have almost halved from their highs in October 2022. In view of existing geopolitical dangers, many mortgage borrowers now prefer planning security,” observes Comparis financial expert Dirk Renkert.

Zurich, October 10, 2024 – As expected, the Swiss National Bank (SNB) has reduced the key interest rate for the third time in a row by 0.25 percentage points from 1.25 percent to 1 percent. The European Central Bank (ECB) had already reduced interest rates by 0.25 percentage points to 3.5 percent, while the US Federal Reserve decided to cut interest rates for the first time in over 4 years – with a jumbo step of 0.50 percentage points 4.75 to 5 percent.

Economic downturn as a danger

Falling crude oil prices and a strong Swiss franc led to falling inflation rates and the SNB significantly revised its forecast for future inflation downwards. The greater danger is the weaker economic development and the fear of prices being too low: Structural problems in Germany and the ongoing real estate crisis in China continue to weigh on the mood of consumers and companies. Weak labor market data in the USA at the beginning of August led to general fears of an economic downturn and a strengthening of the franc, which made imported goods significantly cheaper.

Lower standard rates for fixed-rate mortgages

The benchmark rates for fixed-rate mortgages had been slipping significantly since June and continued their downward trend in the following months. The benchmark rate for 10-year fixed-rate mortgages was 1.81 percent (as of September 30), 0.33 percentage points lower compared to 2.14 percent at the end of June. The benchmark rate for 5-year fixed-rate mortgages was 1.68 percent (as of September 30), 0.36 percentage points lower than at 2.04 percent at the end of June.

At the beginning of the year, the benchmark rates for 10-year and 5-year fixed-rate mortgages were 0.45 percentage points higher at 2.26 percent and 2.13 percent, respectively, compared to the end of September. The yield on 10-year federal bonds was also 0.41 percent at the end of September, 0.25 percentage points lower compared to 0.66 percent at the beginning of the year.

Despite the key interest rate cut: fixed-rate mortgages are still cheaper than Saron mortgages

Even though the interest rate difference between Saron mortgages and fixed-rate mortgages has narrowed again with the third interest rate cut in a row, fixed-rate mortgages are still slightly cheaper than Saron mortgages. The ranges traded after the interest rate cut are as follows: First-tier Saron mortgages cost on average around 1.6 to 2.0 percent, 5-year fixed-rate mortgages around 1.4 to 1.8 percent. 10-year fixed-rate mortgages are trading around 1.5 to 2.0 percent.

«The market expectations that interest rates will continue to fall have had a positive impact on the conditions of fixed-rate mortgages since June and in the following months, causing them to slide. This has meant that despite the SNB cutting interest rates again, the conditions for fixed-rate mortgages are still more favorable than for Saron mortgages. The SNB’s lowered inflation forecast has also fueled hopes that interest rates will continue to fall. Conversely, the negative consequences of increasing escalation in the Middle East, such as the development of oil prices and supply chains, remain difficult to estimate,” says Comparis financial expert Dirk Renkert.

Proportion of long-term fixed-rate mortgages at over 70 percent

The deals from Comparis mortgage partner HypoPlus show a preference for long-term terms. In the third quarter, around 72 percent of all mortgage borrowers opted for a fixed-rate mortgage with a term of 10 years or longer. In the previous two quarters, this proportion was significantly lower at 40 to 50 percent.

Conversely, the share of medium terms (4 to 6 years) halved compared to the previous quarter to around 14 percent. In the second quarter the share was still around 30 percent. The proportion of mortgages with terms of up to three years (including Saron mortgages) also fell significantly from just under 20 percent in the previous quarter to just 7 percent. Around 5 percent of this was accounted for by Saron mortgages.

“In terms of prices, the conditions for 10-year fixed-rate mortgages have almost halved since their peak in October 2022 and are still cheaper than Saron mortgages. Many mortgage borrowers opt for long terms when taking out mortgages because, in times of high geopolitical dangers, they prefer planning security to the risk of interest rate changes,” explains Renkert.

High savings potential when negotiating

Comparis compared the average differences between the reference rate and the top interest rate from HypoPlus for 3-, 5-, 10- and 15-year mortgages as of September 30th and calculated considerable savings potential over the term of the mortgage.

The reference rates calculated by Comparis are published, but still negotiable, average interest rates from over 30 mortgage institutions. The deals actually negotiated by HypoPlus are significantly lower: The best negotiated interest rate for a ten-year fixed-rate mortgage is 1.47 percent (as of September 30, 2024). In contrast, the benchmark rate is 1.81 percent.

Data basis

HypoPlus

Comparis’ mortgage partner, provides the interest rates of the Comparis mortgage barometer. These are based on the benchmark rates of around 30 credit institutions. They are updated daily and in

Interest rate overview

published. Experience shows that the interest rates on mortgage offers are in most cases below the official benchmark rates. The next

Mortgage barometer

will be published in January 2025.

Further information:

Dirk Renkert Financial expert Telephone: 044 360 53 91 Email: [email protected]

comparis.ch/hypoplus

About comparis.ch

With over 80 million visits per year, comparis.ch is one of the most used Swiss websites. The company compares tariffs and services from health insurance companies, insurance companies, banks and telecom providers and offers the largest Swiss online offering for cars and real estate. Thanks to comprehensive comparisons and evaluations, the company brings transparency to the market. In this way, comparis.ch strengthens the decision-making authority of consumers. The company was founded in 1996 by economist Richard Eisler and is privately owned. The company is still majority owned by the founder Richard Eisler. There are no other companies or the state involved in Comparis.