This week we have known the unemployment and social security data for the month of November. The message from the Government has been impregnated with the same triumphalism from which we have been suffering in recent months.

While Europe, the OECD, the IMF and many other international organizations launch notices on an almost weekly basis, from official channels they try to sell a robust recovery, and even higher than the European average. The reality is a very weak evolution, in which the downside risks crystallize one after another … and in which the most disadvantaged is being the ordinary citizen and the Spanish SME.

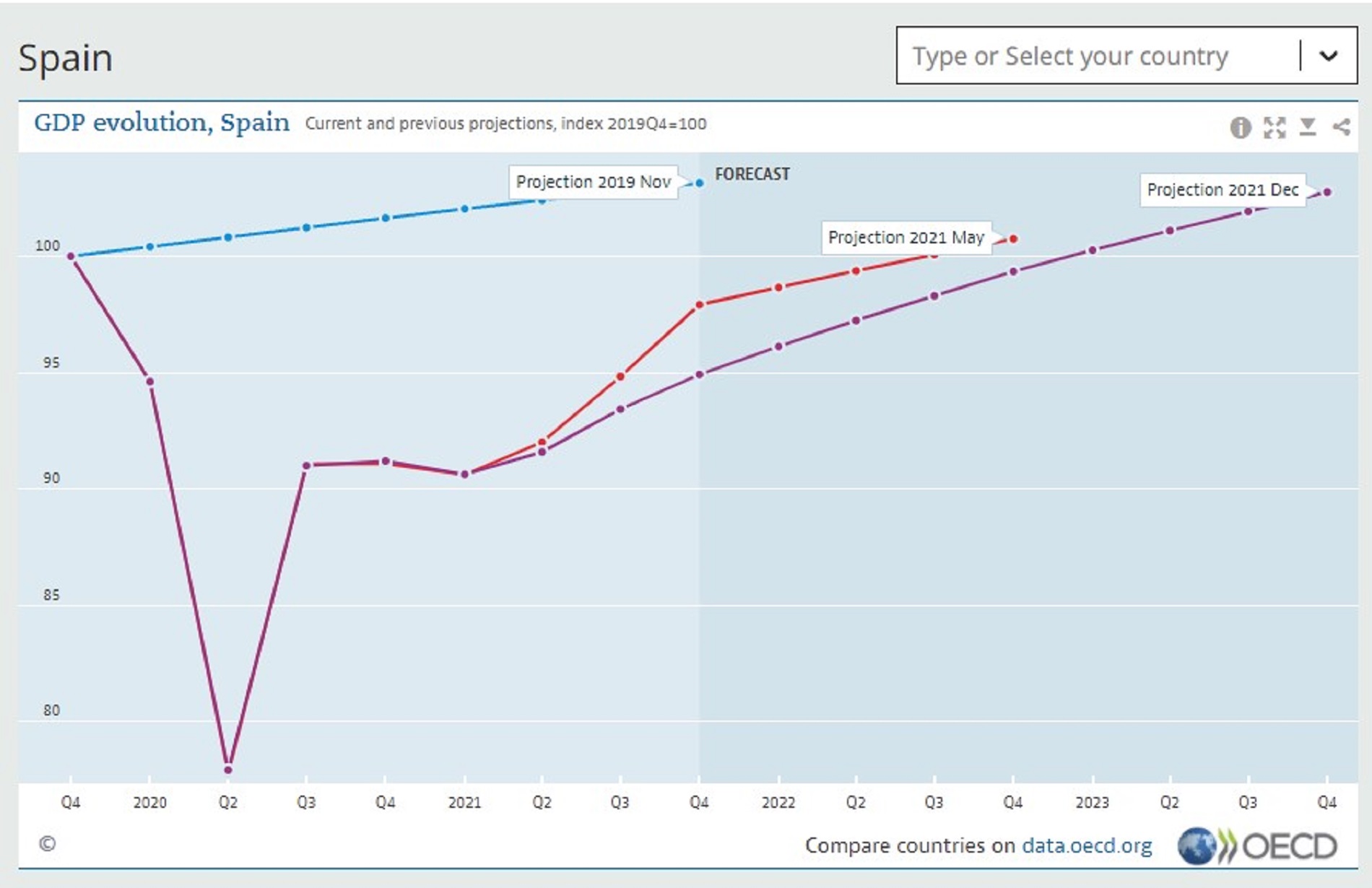

Take a look at this chart from the OECD:

The blue line reflects its growth forecast for the fourth quarter of 2019 (before the pandemic) for the Spanish economy. The red line is the forecast that this organization had in May; and the purple line, the one he made public this week. The conclusion is clear: Spain will not recover its pre-crisis levels of wealth until 2023 —The only European country that occurs in this situation—, we will not recover the wealth levels collected in the trend scenario until 2024…. And the situation is not improving, but is continually getting worse.

This is a real problem, for two reasons: first, because we are going to be the most lagging economy in the Eurozone, and second, and no less important, because we are treating a sick person, with very serious structural problems, like a person healthy who is going through a bump. And that is extremely serious for the potential growth of our country.

Some argue that employment data does not correlate with macroeconomic data. Specifically, there is a current of economic thought that thinks that the calculation of GDP must be revised because the labor market is doing very well and, however, economic evolution is not. Yes, as they read it: there are those who believe that we have to change the formula for calculating national wealth, which is common to all of Europe and to all developed countries, just because the makeup that they are infusing other variables is already insufficient to reflect the real economic situation.

Let’s see some data from the unemployment and social security reports that we have known this week, and surely you have not read:

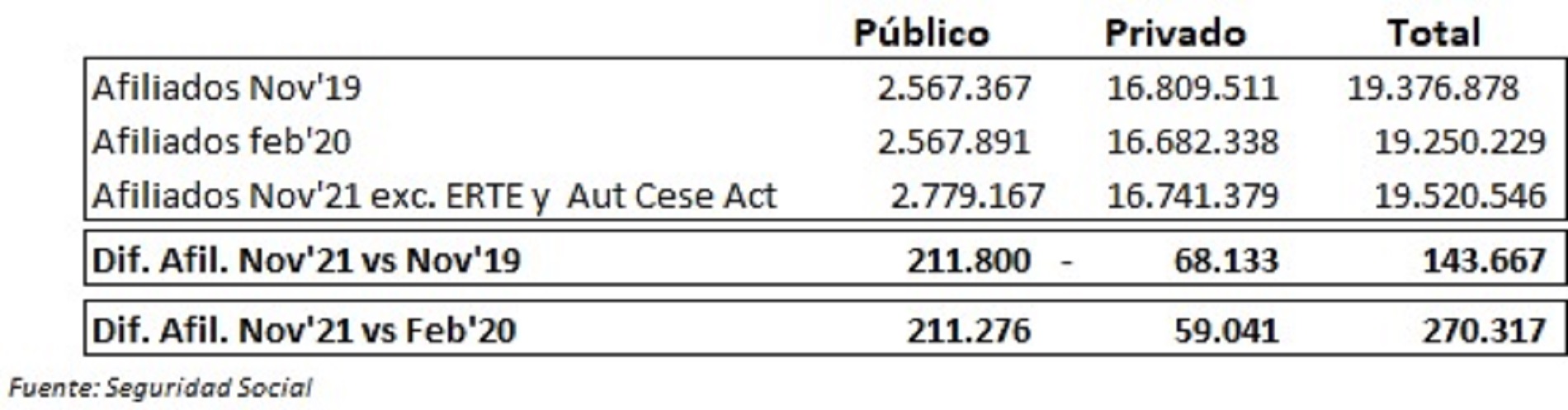

- Spain has taken almost 2 years to recover the levels of effective membership prior to the crisis. If we take into account the people who have been in an ERTE and the self-employed in cessation of activity, the data for November is the first that is above the levels recorded 2 years ago.

- There are 6 autonomous communities that have continued to destroy jobs in the month of November.

- There are still 60,000 companies with employees under their care than before the crisis.

- And there are some sectors, such as agriculture, that maintain their levels of unemployment above 2018.

This in itself is worrying data. But I would like to address two issues that, in my opinion, are of paramount importance when analyzing the labor market. The first is the makeup that the public sector is doing. If we take into account the effective affiliation —that is, excluding ERTE and the self-employed in cessation of activity—, workers in the private sector have fallen by almost 70,000 people with respect to the 2-year levels and account for only 22% of employment Created since February 2020.

I’ll put it another way: Of the 270,000 jobs that have been created since February 2020, 211,000 correspond to the public sector and only 60,000 to the private one. What kind of robust job recovery is this? Among all Spaniards we are paying for the press conferences of our president and our ministers, who use the budget to grace a few.

The second important element is the influence of the Madrid’s community in employment data. Let’s see some figures understandable to all:

- Madrid has created 6 out of 10 jobs created in Spain in November.

- If we take into account the last 3 months, Madrid, which is 14% of the population and 17% of those affiliated with social security, has created at least 50% of national employment.

- In November, it was the region in which unemployment fell the most.

- And, in addition, it has registered the highest affiliation data in its entire history.

The false solvency of the employment data, therefore, is easily dismantled by eliminating the two effects previously exposed. And, if we take them into account, it is much easier to understand the relationship between employment – in the private sector – and macroeconomic developments. Also, the cascade of downward revisions that we are seeing in recent weeks.

The reality of the Spanish economy is that retail sales have been stagnant since the summer, that short-term indicators of economic activity -demand for electricity, vehicle sales, etc.- are also evolving downwards and runaway inflation is eating away at savings from the pandemic and the purchasing power of middle class families. People navigate between a situation of uncertainty about what they live each day and what they consider it should be every time they see any means of communication. Makeup has been working until now, and continues to work, for example, on issues as sensitive as unpaid loans. But that will not last forever, and we are already seeing it with GDP.

We need reforms, and we need to move in the right direction. Any other scenario leads us to the tail wagon of the financial crisis upside down.

– .