–

–

In Europe, at the time of writing, the FTSE was up 0.17%, the DAX down 0.66%, the CAC down 0.55%, Germany’s 10-year yield was up of 0.1122 to 1.214 earlier in Asia, the Nikkei down 0.04%. HSI up 0.05% China Shanghai SSE down -0.59% Singapore Straits Times down -0.82% Japan 10Y JGB Yield up 0.0011 to 0.201.

Canadian retail sales increased 1.1% mom in June. Main sales increased by 0.2% m / m.

Canadian retail sales increased 1.1% on a monthly basis CAD 63.1B in June Above expectations at 0.4% m / m. This is also the sixth consecutive month increase. Sales increased in eight of the 11 sub-stores, accounting for 76.8% of retail. main retail sales Not including Automotive and components service stations, up 0.2% m / m

in the forward estimate Retail sales fell -2.0% mom in July.

UK retail volumes increased 0.3% mom in July.

In terms of volume, UK retail sales increased 0.3% mom in July. Better than expected -0.2% m / m Classic car sales increased 0.4% m / m YoY. Retail sales fell -3.4% yoy, while used car sales fell -3.0% yoy.

In terms of value, retail sales increased 1.3% m / m, 7.8% yoy, while classic car sales increased 1.4% m / m, 5 , 7% year over year.

From Germany, the PPI increased 5.3% mom, 37.2% yoy in July. Above expectations at 0.5% m / m, 31.5% y / y.

Consumer confidence in the UK Gfk falls to -44, an all-time low

UK Gfk consumer confidence fell from -41 to -44 in August. which has reached another record Personal financial situation in the next 12 months has fallen from -26 to -31 The overall economic situation in the next 12 months has fallen from -57 to -60, establishing a new all-time low.

Joe Staton, GfK’s director of client strategy, said: “The overall index score fell three points in August to -44, the lowest since the record start in 1974. All measures were at discount. reflects strong concern as the cost of living has skyrocketed. Anger over the UK economy was the main driver of these results. “

Japan’s CPI rose 2.4% yoy, the highest since 2014.

Japan’s main CPI increased from 2.4% yoy to 2.6% yoy in July. Beyond expectations of 2.2% yoy, core CPI (all items except fresh food) increased from 2.2% yoy to 2.4% yoy, in line with expectations. Core-core CPI (all items except food, energy) increased by 1.0% year on year. It was 1.2% yoy, above expectations at 0.6% yoy.

Core inflation has now exceeded the BoJ’s 2% target for four consecutive months. and peaked since December 2014. Key reads have been the fastest since December 2015, while key reads have been the strongest since 2008.

Both Prime Minister Fumio Kishida and BoJ Governor Haruhiko Kuroda have called for hefty wage increases to ensure sustained inflation. But markets are expecting pressure on the BoJ to pursue monetary policy if the CPI hits 3%.

New Zealand’s merchandise exports increased 16% yoy in July. imports up 26% year on year

New Zealand’s merchandise exports increased 16% yoy to NZD 6.7 billion in July. Goods imports increased 26% yoy to NZD 7.8 billion. The trade deficit stood at NZ $ 1.1 billion, comparing expectations for a NZD 105 million surplus.

China led monthly exports up 13%, exports to Australia fell -1.1%, the US increased 5.8%, the EU increased 7.5%, Japan increased by 18%, imports from China increased by 19%, the EU added a 3.0% increase, Australia up by 16%, the US up by 34% and Japan up by 54%.

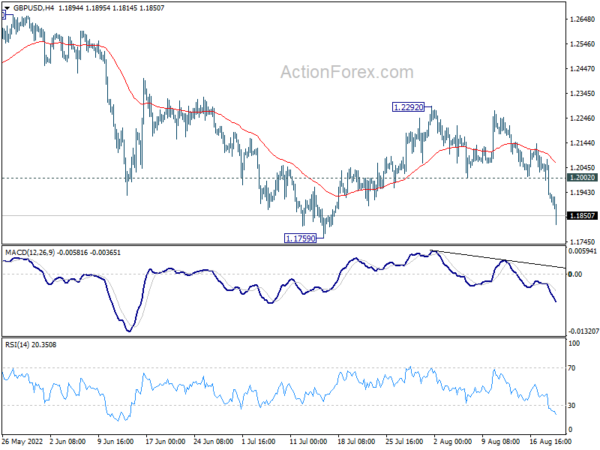

GBP / USD Daytime pattern

Daily rotation: (S1) 1.1876; (R) 1.1978 (R1) 1.2033; more than…

Autumn GBP / USD It accelerated to the low of 1.1814 and intraday bias remains to the downside for the retest of the 1.1759 support. The firm break will resume a bearish trend. The next target is the low of 1.1409. Conversely, the support above the 1.2002 resistance will first shift the intraday trend to neutral. But the risk will remain to the downside as long as there is resistance at 1.2292.

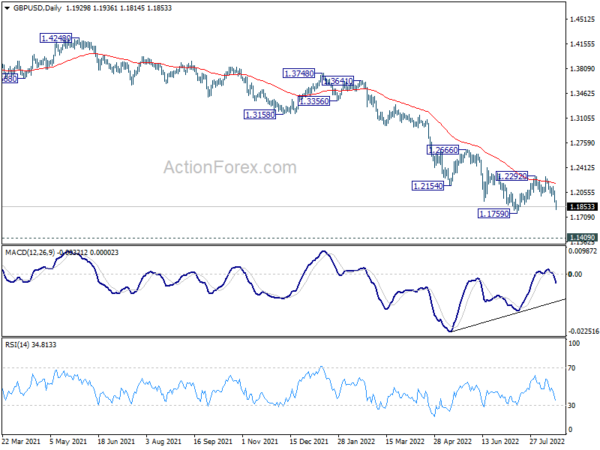

In the big picture, a drop from 1.4248 (2018 high) could be a leg in the 1.1409 pattern (2020 low) or a reversal of a long-term downtrend. A deeper decline is expected as long as resistance at 1.2666 is present. The next target is the low of 1.1409. However, a breakout at 1.2666 will bring back a strong rally to the 55-week EMA (now at 1.2897).

Update economic indicators

| GMT |

Ccy |

activities |

real |

prophecy |

Previous one |

correct |

| 22:45 |

NZD |

Trade Balance (NZD) July |

-1092M |

105 million |

-701 million |

-1102M |

| 23:01 |

GBP |

Consumer confidence GfK ส. ค |

-44 |

-42 |

-41 |

|

| 23:30 |

JPY |

Core National CPI Y / Y Jul. |

2.40% |

2.40% |

2.20% |

|

| 06:00 |

EUR |

Germany PPI M / M July |

5.30% |

0.50% |

0.60% |

|

| 06:00 |

EUR |

Germany PPI a / a jul. |

37.20% |

31.50% |

32.70% |

|

| 06:00 |

GBP |

Retail Sales M / M Jul. |

0.30% |

-0.20% |

-0.10% |

-0.20% |

| 06:00 |

GBP |

Retail Sales Y / Y / Jul |

-3.40% |

-3.30% |

-5.80% |

-6.10% |

| 06:00 |

GBP |

Retail sales of former M / M fuel Jul. |

0.40% |

-0.20% |

0.40% |

0.20% |

| 06:00 |

GBP |

Retail sales of former P / P fuel. Jul. |

-3.00% |

-2.80% |

-5.90% |

-6.20% |

| 06:00 |

GBP |

Public loan (GBP) Jul |

4.2B |

25.3B |

22.1B |

20.1B |

| 8:00 in the morning. |

EUR |

Eurozone Current Account (EUR) Jun |

4.2B |

-3.3B |

-4.5B |

-6.9B |

| half past twelve |

CAD |

Retail Sales M / M Jun |

1.10% |

0.40% |

2.20% |

2.30% |

| half past twelve |

CAD |

Retails as M / M Automobiles Jun |

0.80% |

0.90% |

1.90% |

|

–