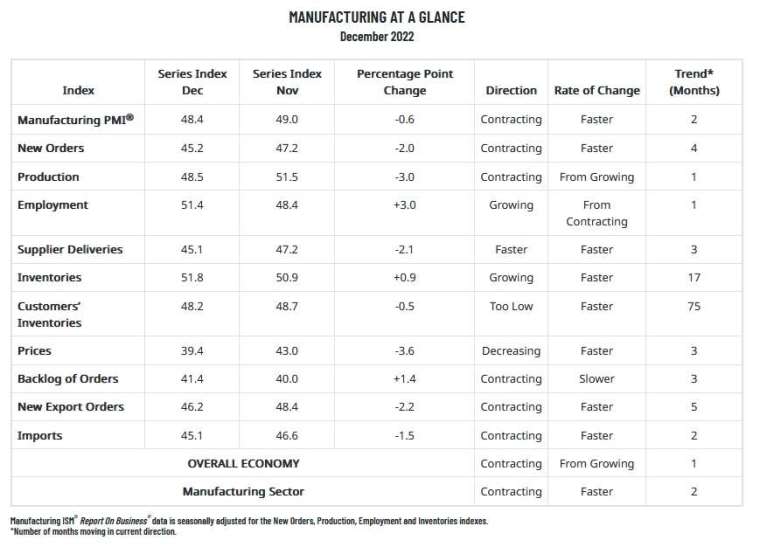

The ISM manufacturing index released by the United States on Wednesday (4) fell to 48.4 in December last year, decreasing for the second consecutive month, lower than market expectations of 48.5 and lower than 49.0 in November, the lowest since May 2020. For all of last year, the index fell by 10.4 points, the largest annual decline since 2008. The good news is that commodity inflation continues to decline, with the index in prices falling to the lowest level in more than two and a half years due to weakening demand.

December US ISM Manufacturing Index Breakdown:

- The new orders index returned 45.2, the previous value of 47.2

- The production index reported 48.5, the previous value was 51.5

- The employment index returned 51.4, the previous value of 48.4

- The Supplier Delivery Index reported 45.1, the previous value of 47.2

- The inventories index reported 51.8, the previous value was 50.9

- The customer’s inventory index reported 48.2, the previous value was 48.7

- The price index reported 39.4, the previous value of 43.0

- The Backorders Index came in at 41.4, up from 40.0

- The export orders index reported 46.2, the previous value of 48.4

- The commodity import index reported 45.1, the previous value was 46.6

Looking at the data in detail, the new orders index in December stood at 45.2, down from the previous value of 47.2, the minimum since May 2020, and decreased for the fourth consecutive month, while the production index also fell from 51.5 in November to 48.5 In the contraction interval, two weak data point to a further weakening of demand in the future.

In December, the export orders index was brought back to 46.2, still down on the previous value of 48.4; the import index of commodity import index was reported as 45.1, lower than the previous value of 46.6, and the two data fell into the narrowing range.

It is worth noting that the price index in December recorded 39.4, a new low since April 2020, far below market expectations of 42.9 and the previous value of 43. This is the ninth month consecutive decline in the price index, the longest since 1974 – 1975. The longest decline.

On the labor market front, the employment index rose to 51.4 from the previous value of 48.4 in December, returning to the expansion range and reaching a new high in four months. Furthermore, the Supplier Delivery Index fell to 45.1 in December from 47.2 the previous month. Contracting demand combined with loosening supply chains has seen suppliers deliver faster, the lowest level since March 2009.

According to earlier data released by S&P Global, the final value of the Markit Manufacturing Purchasing Managers Index (PMI) in the United States in December was 46.2, the initial value was 46.2, still in the contraction range, and it is also a new low since the outbreak of the new corona epidemic. The trend given by the ISM manufacturing index is in line with that.

The market analysis showed that the ISM manufacturing index showed that consumer spending preferences have shifted towards services and goods, along with rising interest rates and weakening global economic activity, putting pressure on factories. Heightened uncertainty and plummeting demand suggest the challenges manufacturers will face will continue this year.

Market reaction

Bad news in economic data is no longer good news for markets. At the moment, the market is generally concerned that a weakened economy will drag down US stock earnings and hit the market. Following the release of the ISM manufacturing index for December in the US, major US stock indexes once fell but then resumed their gains.

before the deadline,Dow Jones Industrial Averagerose more than 80 points or nearly 0.3%,Nasdaq Composite Indexrose more than 50 points or nearly 0.6%,S&P 500 index+0.6%,Semiconductor PhiladelphiaThe index is up more than 2%.