A stabilization of fixed rate mortgages is looming according to MoneyPark experts.

Macroeconomic situation

Rampant inflation due to exploding energy costs…

The second quarter was marked by inflation of more than 8% in the United States, a record since 1981. At the time, the country was in recession due to the oil crisis. In the euro zone, the inflation rate also crossed the 8% mark in May, which corresponds to a level 4 times higher than in May 2021. The general rise in prices is mainly due to the increase in energy prices (gas, oil, electricity) and shortages of key foodstuffs (eg wheat).

…and increase in distribution problems

The continuation of the “zero Covid” policy in China, the war in Ukraine and the inaccessibility of infrastructure in Russia, Belarus and Ukraine, including important Ukrainian ports on the Black Sea, have led to new difficulties in supply and a rise in the prices of semi-finished products and raw materials. These eventually impacted the end prices of many consumer products.

First increases in key interest rates by the FED and the SNB

On March 16, May 4 and June 15, 2022, the Fed’s long-awaited first measures to fight inflation were introduced: in a month and a half, the interest rate rose from 0.25- 0.5 % at 1.5-1.75%. Surprisingly, the SNB did not wait for the signal from the ECB as in the past, although inflation in Switzerland was “only” 2.9% in May. On June 16, the SNB raised its key rate by 0.5 points to -0.25% and announced further increases by the end of the year. The objective of the increase in financing costs is to reduce the circulation of money, and therefore inflation. This step has been postponed for a long time, because the economy needed liquidity to recover from the coronavirus crisis and for the indebtedness of the States to be still sustainable.

Switzerland: confidence in economic development down

In December 2021, SECO forecast GDP growth of 3% for 2022. After an initial revision in March, growth was revised downwards (2.6%) in mid-June. One of the main elements is that Switzerland, as an export-oriented country, is highly dependent on global demand, which is expected to be massively reduced over the next two years, due to the factors described above.

Evolution of interest rates

Interest rates continue to rise, especially for short maturities

The roughly 50 basis point increase in mortgage rates in the first quarter was historically high. In the second quarter, it was even twice as high, around 100 bps! The responsible factors are the increase in the key rates of the Fed and the SNB and that of the SWAP rates due to inflation. In the second quarter, short- and medium-term mortgages rose more sharply than long-term ones, perhaps putting an end to the significant jumps in rates.

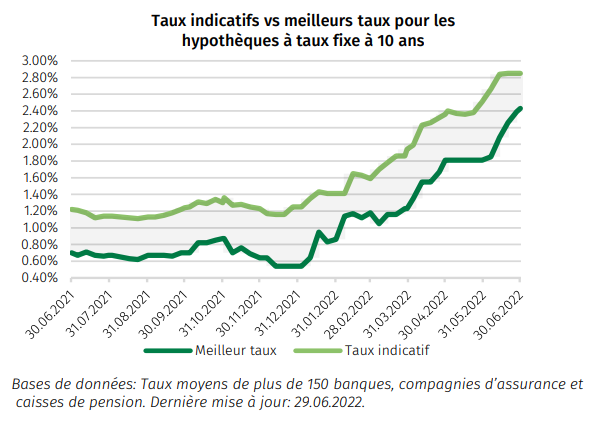

The range of offers is narrowing

The best rate for a 10-year mortgage rose 60 basis points in June to around 2.4%, while the most expensive offer rose only around 30 basis points. Since the most expensive suppliers have not yet crossed the psychological threshold of 3%, the range of offers has therefore not been so narrow for a long time, with less than one percent. It’s probably only a matter of time before the first providers charge 3% for a 10-year fixed mortgage.

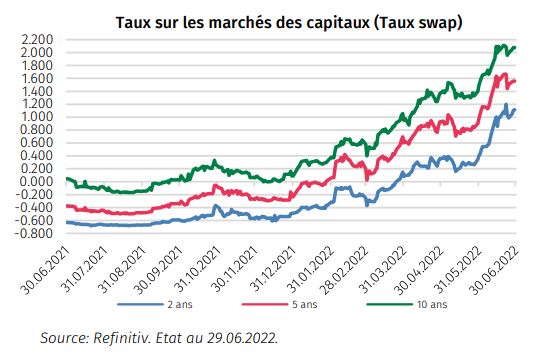

Capital market rates continue to climb inexorably

Capital market rates increased further in the second quarter (+ c. 100 bps or 1%), depending on the maturity. In mid-December, the 10-year SWAP rate was still at 0%, at the end of June it was around 2%. In June, it rose 60 points, driven by the Fed’s rate hike. While in the first quarter, long maturities rose more strongly, the 2-year SWAP rate posted an increase of around 100 points in the second quarter. The last time the 10-year SWAP rate was above 2% was in July 2011. This illustrates the historical magnitude of the level of interest rates.

Forecast of the evolution of rates

A stabilization of fixed rate mortgages is looming

After a rise in interest rates of 1.5% in 6 months, there are signs of stabilization of interest rates for fixed mortgages at their current level. The hikes in key rates announced by national banks for the next few months should be largely integrated into current mortgage rates. If, however, inflation continues to rise, mortgages could still rise by around 20 to 30 basis points. However, there is still a considerable risk that inflation will turn into a major economic slowdown, which could prompt central banks to delay or even suspend their rate hikes. A slight increase or a slight decrease in mortgage rates seems to us to be the most realistic scenario for the second half.

Will mortgage market mortgages be more expensive in the second half?

Mortgage borrowers who rely on SARON mortgages have so far been spared from rising rates. As long as the key interest rate in Switzerland does not exceed 0%, nothing will change. For two weeks, only 25 points are missing to reach this rate of 0%. Therefore, any further rise in interest rates would be passed on to SARON. In our view, this scenario could materialize in the fourth quarter, however it does not make SARON less attractive.

Recommendations

- The level of interest rates could continue to rise in the weeks and months to come. It is therefore important to be concerned upstream of the renewal of a mortgage and then to quickly seize the opportunities.

- Small banks, insurance companies and pension funds that have sufficient deposits and do not have to refinance themselves on the capital market can gain market share by offering attractive interest rates. It is worth including these supplier groups when comparing.

- Those who have sufficient risk capacity can rely on SARON mortgages. Admittedly, a rise again seems only a matter of time, but for the time being, the attractiveness of this product compared to long-term fixed mortgages should remain high.

–

")