Faced with the coronavirus pandemic, Washington has adopted a series of massive plans to support the American economy which have widened public deficits. After reaching a record level of $ 3.132 billion in 2020, or nearly 15% of GDP, the federal budget deficit is expected to stand at $ 2.770 billion in 2021, or 12.5% of GDP.

At the same time, the current account deficit, which roughly corresponds to the negative balance between the value of exports of goods and services and the value of imports of goods and services, widened to almost 3% of GDP in 2020. According to forecasts from the International Monetary Fund and the Organization for Economic Co-operation and Development, the deterioration of the US external accounts should also continue in 2021 and 2022 (the current account deficit could reach 4% of GDP in 2022).

The expression “Twin Deficits”, which designates the simultaneous increase in the budget deficit and the current account deficit, therefore seems to apply in the current context. In an article published in 2020, we showed that there was a positive long-term relationship between these deficits: an increase of one dollar in the US budget deficit is accompanied by a 0.40 dollar increase in the US current account deficit.

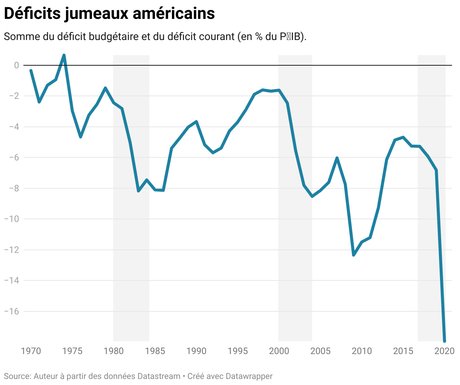

But is the current excavation transitory, as it may have been in recent decades (see graph below)? Or does it mark the beginning of a new phase of degradation which could constitute a danger for the United States, this time because of a reduced capacity to mobilize foreign savings?

The status of the dollar

During the first half of the 1980s, the reduction in taxes resulting mainly from the application of the Economic Recovery Act (August 1981), combined with the increase in public expenditure, had led to a sharp increase in the deficit. US federal budget, which fell from 2.6% of GDP in 1980 to 5% in 1985. Over the same period, during which the term “twin deficits” appeared, the external deficit widened sharply for reach 3.2% of GDP in 1985.

The United States subsequently experienced two other similar episodes. The first took place in the early 2000s. At the time, alongside high and persistent current account deficits, public accounts deteriorated under the combined effect of the war in Iraq and numerous tax cuts granted by the administration of George W. Bush in order to revive economic activity damaged by the bursting of the Internet bubble.

The second episode began in 2017. While the American economy was close to full employment, President Donald Trump adopted an expansionary budgetary policy, by reducing taxes (application of the major tax reform “Tax cuts and Jobs Act” adopted in December 2017) and by increasing public spending. This procyclical fiscal policy then caused a widening of the budget deficit and the current deficit (the two deficits reached 4.6% and 2.2% of GDP respectively in 2019).

So far, the United States has enjoyed “no-tears and no-hitches financing” of its twin deficits. Given the dollar’s status as an international currency, international investors, both private and official, have in fact agreed to add Treasury securities issued by the United States to their portfolios to finance their double deficit.

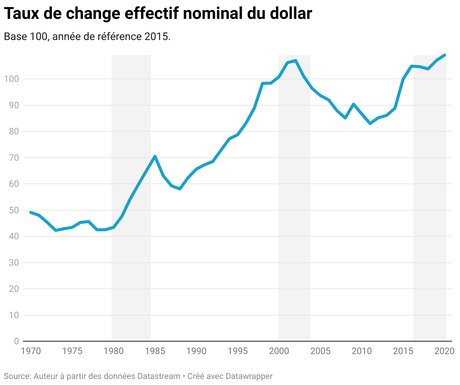

The rise in net capital inflows into the United States during the episodes of twin deficits thus caused, at least initially, an appreciation of the dollar which in turn led to a deterioration in the American current account. The following graphs show the positive correlation between twin deficits and the dollar rate (between 1980 and 1985, then between 2000 and 2002 and finally between 2018 and 2020).

The so-called “Bretton-Woods 2” international monetary system, in effect between the end of the 1990s and the beginning of the 2010s, notably made it possible to finance twin American deficits by China, and to a lesser extent, by others. emerging Asian countries.

For its part, to prevent its currency from appreciating under the effect of colossal trade surpluses, China has accumulated large foreign exchange reserves in dollars (up to $ 4 trillion), which have been invested mainly in dollar assets, especially treasury securities. For years, the Middle Kingdom was thus the largest holder of US Treasury bonds (at the end of 2013, it held $ 1,312 billion, or 23% of the total held outside the United States). China has thus made a significant contribution to the financing of US current account and budget deficits.

Fewer foreign investors

Since the onset of the health crisis, the decline in the share of treasury bills held by non-residents (minus 6 points between March 2019 and September 2021) was offset by the increase in that held by the Federal Reserve (Fed). However, the process of gradually reducing asset purchases by the Fed (“tapering”), which began last November, will force the US Treasury to borrow more from its other domestic and foreign creditors.

Since the end of the 1980s, the trend has been towards a reduction in the proportion of Treasury bills held by non-residents. After reaching a high point of 58% in 2008, this share gradually fell to 33% in September 2021.

However, the increase in the issuance of US treasury bills on the markets, while demand remains unchanged, could cause the price of bonds to fall, and therefore a rise in long-term interest rates. Over the next few years, the US federal budget will then have to focus primarily on reducing the Treasury’s financing requirement.

Twin deficits remaining too high and / or expected to persist over too long a period could thus, over time, erode the confidence of international investors in securities denominated in dollars.

There are good reasons today to consider that, given the size of the US twin deficits, the US savings rate and current account variables may still exert a significant influence on the economy for some time to come. US long rates and exchange rates. According to some forecasters, these variables could even weigh more heavily in the future than monetary policy measures, such as the end of accommodative quantitative easing policies in the United States and in the euro area.

![]() _______

_______

Through , Professor of international economics, University of Bordeaux

The original version of this article appeared on The Conversation.