Share

![]()

X

kakaotalk

![]()

![]()

Entered 2024.10.20 06:00 Modified 2024.10.20 06:00 Reporter Hwang Hyun-wook ([email protected])

‘Magnifying Glass’ review to respond to insurance fraud

There is a possibility of inconvenience to unspecified subscribers

“There is nothing we can do to respond to insurance fraud.”

Insurance image. ⓒPixabay

It was found that the amount of insurance money that domestic non-life insurance companies have to pay to subscribers is close to 26 trillion won. The non-life insurance industry’s position is that in order to respond to insurance fraud that is becoming more sophisticated day by day, there is no choice but to put a magnifying glass on the payment process and take a closer look.

However, some point out that this may make the process of receiving insurance money inconvenient and cause consumer dissatisfaction.

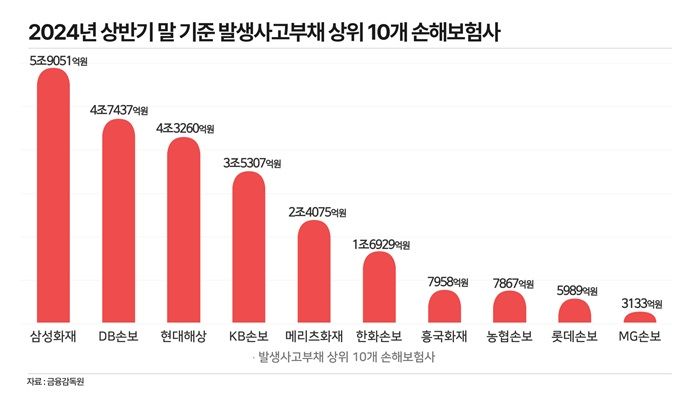

According to the Financial Supervisory Service on the 20th, the total accident liabilities of 17 non-life insurance companies as of the end of the first half of this year were 25.8681 trillion won. Compared to the same period last year, it decreased slightly (0.7%).

Occurrence liability is an amount that is held as a liability by the insurance company because the reason for paying the insurance money agreed upon in the contract has already occurred, but has not yet been paid. This includes insurance payments scheduled to be paid and costs under review for payment.

By non-life insurance company, Samsung Fire & Marine Insurance’s accident liabilities reached the highest at KRW 5.9051 trillion, an increase of 6.5% compared to the same period. DB Insurance also increased by 10.0% to KRW 4.7437 trillion. In the case of Hyundai Marine & Fire Insurance, it decreased by 3.2% to 4.326 trillion won.

In addition, ▲KB Non-Life Insurance KRW 3.5307 trillion ▲Meritz Fire & Marine Insurance KRW 2.4075 trillion ▲Hanwha Non-life Insurance KRW 1.6929 trillion ▲Heungkuk Fire & Marine Insurance KRW 795.8 billion ▲NH Nonghyup Non-Life Insurance KRW 786.7 billion ▲Lotte Non-Life Insurance KRW 598.9 billion ▲MG Non-life Insurance KRW 313.3 billion It appeared.

Top 10 non-life insurance companies in accident liabilities as of the end of the first half of 2024. ⓒDalian Reporter Hwang Hyun-wook

Insurance fraud and over-treatment are the reasons why non-life insurance companies are in no hurry to pay insurance claims.

The amount of insurance fraud detected is around 1 trillion won, reaching a record high every year. Last year, the amount of insurance fraud detected was 1.1164 trillion won, and the number of people caught was 109,522.

An insurance industry official said, “As the recent economic recession continues, insurance frauds involving small amounts of money are on the rise, so insurance companies are carefully examining payment applications.” He added, “The Insurance Fraud Prevention Act has been revised, but as the law is in place, there is still a lot to do in the field.” “There is an atmosphere in which screening is being strengthened,” he said.

Experts say that, excluding the unusual number of applications for insurance benefits, the review period should be shortened in small cases of repeated applications for the same disease.

Seo Ji-yong, a professor of business administration at Sangmyung University, said, “In foreign countries, routine insurance payments are made fairly quickly and are only reviewed in detail in unusual cases. It is understandable that insurance companies are being strict as insurance fraud is increasing, but good consumers “There are cases where people are suffering damage,” he said.

He went on to suggest, “Insurance companies should approach from a long-term perspective, as insurance companies’ credibility will decrease if insurance payment payments are indiscriminately prolonged.”

©Dailyan Co., Ltd. Unauthorized reproduction and redistribution prohibited

0

0

‘;

replyDiv.outerHTML = comment;

}

// var imageDiv = document.getElementsByClassName(‘figure’)[0]; // var lineBanner = document.getElementById(‘innerLineBanner’); // var squareBanner1 = document.getElementById(‘innerSquareBanner1’); // var squareBanner2 = document.getElementById(‘innerSquareBanner2’); // var squareBanner3 = document.getElementById(‘innerSquareBanner3’); // var squareBanner4 = document.getElementById(‘innerSquareBanner4’); // var boxBanner = document.getElementById(‘innerBoxBanner’); // var boxBanner2 = document.getElementById(‘innerBoxBanner2’); // const articleP = document.querySelectorAll(‘.article p’); // let pArray = [];

// for(let i = 0; i ‘ && articleP[i].parentElement.className != ‘inner-subtitle’){

// pArray.push(articleP[i])

// }

// }

// // console.log(pArray, pArray.length)

// let tmpIdx = 1;

// if(pArray.length > 5){

// tmpIdx = 4;

// }else if(pArray.length > 3){

// tmpIdx = pArray.length – 1;

// }else{

// tmpIdx = pArray.length – 1;

// }

// if(tmpIdx > 3){

// if(boxBanner){

// if(pArray[tmpIdx].previousElementSibling && pArray[tmpIdx].previousElementSibling.innerHTML == ‘

‘){

// pArray[tmpIdx].previousElementSibling.remove();

// }

// pArray[tmpIdx].parentElement.insertBefore(boxBanner, pArray[tmpIdx]); // } // if(boxBanner2){ // if(pArray[tmpIdx-3].previousElementSibling && pArray[tmpIdx-3].previousElementSibling.innerHTML == ‘

‘){

// pArray[tmpIdx-3].previousElementSibling.remove();

// }

// pArray[tmpIdx-3].parentElement.insertBefore(boxBanner2, pArray[tmpIdx-3]); // } // if ( squareBanner3 ){ // pArray[tmpIdx-2].parentElement.insertBefore(squareBanner3, pArray[tmpIdx-2]); // } // if ( squareBanner4 ){ // pArray[tmpIdx-2].parentElement.insertBefore(squareBanner4, pArray[tmpIdx-2]);

// }

// }else if(tmpIdx == 3){

// if(boxBanner){

// if(pArray[tmpIdx].previousElementSibling && pArray[tmpIdx].previousElementSibling.innerHTML == ‘

‘){

// pArray[tmpIdx].previousElementSibling.remove();

// }

// pArray[tmpIdx].parentElement.insertBefore(boxBanner, pArray[tmpIdx]); // } // if(boxBanner2){ // if(pArray[tmpIdx-2].previousElementSibling && pArray[tmpIdx-2].previousElementSibling.innerHTML == ‘

‘){

// pArray[tmpIdx-2].previousElementSibling.remove();

// }

// pArray[tmpIdx-2].parentElement.insertBefore(boxBanner2, pArray[tmpIdx-2]); // } // if ( squareBanner3 ){ // pArray[tmpIdx-1].parentElement.insertBefore(squareBanner3, pArray[tmpIdx-1]); // } // if ( squareBanner4 ){ // pArray[tmpIdx-1].parentElement.insertBefore(squareBanner4, pArray[tmpIdx-1]);

// }

// }else if(tmpIdx == 2){

// if(boxBanner){

// if(pArray[tmpIdx].previousElementSibling && pArray[tmpIdx].previousElementSibling.innerHTML == ‘

‘){

// pArray[tmpIdx].previousElementSibling.remove();

// }

// pArray[tmpIdx].parentElement.insertBefore(boxBanner, pArray[tmpIdx]); // } // if(boxBanner2){ // if(pArray[tmpIdx-1].previousElementSibling && pArray[tmpIdx-2].previousElementSibling.innerHTML == ‘

‘){

// pArray[tmpIdx-2].previousElementSibling.remove();

// }

// pArray[tmpIdx-2].parentElement.insertBefore(boxBanner2, pArray[tmpIdx-2]); // } // if ( squareBanner3 ){ // pArray[tmpIdx-1].parentElement.insertBefore(squareBanner3, pArray[tmpIdx-1]); // } // if ( squareBanner4 ){ // pArray[tmpIdx-1].parentElement.insertBefore(squareBanner4, pArray[tmpIdx-1]);

// }

// }else if(tmpIdx == 1){

// if(boxBanner){

// if(pArray[tmpIdx].previousElementSibling && pArray[tmpIdx].previousElementSibling.innerHTML == ‘

‘){

// pArray[tmpIdx].previousElementSibling.remove();

// }

// pArray[tmpIdx].parentElement.insertBefore(boxBanner, pArray[tmpIdx]); // } // if(boxBanner2){ // if(pArray[tmpIdx].previousElementSibling && pArray[tmpIdx].previousElementSibling.innerHTML == ‘

‘){

// pArray[tmpIdx-1].previousElementSibling.remove();

// }

// pArray[tmpIdx-1].parentElement.insertBefore(boxBanner2, pArray[tmpIdx-1]); // } // if ( squareBanner3 ){ // pArray[tmpIdx].parentElement.insertBefore(squareBanner3, pArray[tmpIdx]); // } // if ( squareBanner4 ){ // pArray[tmpIdx].parentElement.insertBefore(squareBanner4, pArray[tmpIdx]);

// }

// }else{

// if(boxBanner){

// pArray[tmpIdx].parentElement.insertBefore(boxBanner, pArray[tmpIdx]);

// pArray[tmpIdx].parentElement.insertBefore(pArray[tmpIdx]boxBanner); // } // if(boxBanner2){ // pArray[tmpIdx].parentElement.insertBefore(boxBanner2, pArray[tmpIdx]);

// pArray[tmpIdx].parentElement.insertBefore(pArray[tmpIdx]boxBanner2);

// }

// if(squareBanner3){

// pArray[tmpIdx].parentElement.insertBefore(squareBanner3, pArray[tmpIdx]); // } // if ( squareBanner4 ){ // pArray[tmpIdx].parentElement.insertBefore(squareBanner4, pArray[tmpIdx]);

// }

// }

// // console.log(imageDiv)

// if(imageDiv){

// if(lineBanner){ imageDiv.appendChild(lineBanner) }

// if(squareBanner1){

// imageDiv.parentElement.insertBefore(squareBanner1, imageDiv)

// imageDiv.parentElement.insertBefore(imageDiv, squareBanner1)

// }

// if(squareBanner2){

// imageDiv.parentElement.insertBefore(squareBanner2, imageDiv)

// imageDiv.parentElement.insertBefore(imageDiv, squareBanner2)

// }

// }else{

// lineBanner.remove();

// squareBanner1.remove();

// squareBanner2.remove();

// }

}

function gotoReply(){

const footerDom = document.querySelector(‘footer’);

const replyDom = document.querySelector(‘#lv-container’);

// console.log(document.body.scrollHeight, screen.height, footerDom.clientHeight, replyDom.clientHeight)

window.scrollTo(0, document.body.scrollHeight – footerDom.clientHeight – replyDom.clientHeight + 55)

// console.log(window.scrollY)

}

function openShares(e) {

document.getElementById(‘shareDiv’).style.visibility

= document.getElementById(‘shareDiv’).style.visibility == ‘visible’ ? ‘hidden’ : ‘visible’

// document.getElementById(‘btns_share’).style.visibility

// = document.getElementById(‘btns_share’).style.visibility == ‘visible’ ? ‘hidden’ : ‘visible’

}

var size=”width=626 height=436″;

function shareFacebook() {

window.open(‘ + window.location.href, ‘_blank’, size);

}

function shareKakaoStory() {

window.open(‘ + window.location.href, “_blank’, size);

}

function shareTwitter() {

window.open(‘ + window.location.href, “_blank’, size);

}

function shareBand() {

//coming soon

}

//

//

function socialShare(type){

var snsTitle = encodeURIComponent(document.querySelector(‘.news-contents .title’).innerHTML);

var snsUrl = encodeURIComponent(window.location.href);

var snsCopy = encodeURIComponent(“데일리안”);

var opensns = “”;

if(type == “facebook”){

opensns +=”

opensns += “&&t=”+snsTitle;

openSnsWin(opensns);

} else if(type == “band”){

opensns += “””+snsTitle+””:”+snsUrl;

opensns += “&new_post=”+snsCopy;

openSnsWin(‘

}else if(type == “kakaostory”){

opensns +=”+snsUrl;

openSnsWin(opensns);

}

else if(type == “twitter”) {

opensns += ”

openSnsWin(opensns)

}else if(type == “url”){

var urlbox = document.getElementById(‘urlData’);

urlbox.value = location.href;

urlbox.select();

var result = document.execCommand(“copy”);

alert( ‘URL 이 복사 되었습니다.’);

}

}

function openSnsWin(opensns) {

var winObj;

winObj = window.open(opensns,””,”width=560, height=520, scrollbars=yes, resizable=yes”);

}

![Should I run comfortably on Korean roads? Renault’s ambitious project that overcomes various negative factors [주말車담]](https://pds.joongang.co.kr/news/component/htmlphoto_mmdata/202410/19/220ebfbd-82da-499b-b06a-d14ae4b8e870.jpg "Should I run comfortably on Korean roads? Renault’s ambitious project that overcomes various negative factors [주말車담]")